Energy Technology Perspectives 2026 positions heat pumps and air conditioning as mature, scalable technologies with massive system impact. It states that heat pumps are central to electrification and decarbonisation of buildings but also for the industrial sector to improve resilience and reduce emissions. Air conditioning is unavoidable in a warming world and must be made dramatically more efficient according to the report. The report concludes heat pumping technologies expose supply chain and industrial competitiveness challenges and that policy design is now the primary limiting factor for further deployment of efficient heat pump and air conditioning technologies.

International Energy Agency published the 2026 issue of one it the agencies flagship publications, the Energy Technology Perspectives (ETP 2026), on March 26. The 2026 edition aims to provide a comprehensive update on selected key energy technologies, heat pumping technologies being one of them.

The report examines demand-side dynamics for energy technologies, such as deployment trends and policy developments, but also supply-side factors, including manufacturing capacity and trade flows. This year’s edition puts a special focus on vulnerabilities in energy technology supply chains and industrial competitiveness, analysing manufacturing cost structures and industrial policy impacts.

Strategic importance for electrification and decarbonisation

Heat pumps and air conditioning (AC) systems emerge in ETP 2026 as core technologies of the “Age of Electricity” underpinning both building decarbonisation and also a rising electricity demand. The report views heat pumps and AC as closely linked markets, sharing technology platforms, components (notably compressors), and manufacturing bases, while serving different climate and policy needs.

Deployment trends: strong longterm growth with shortterm volatility

Heat pumps (buildings)

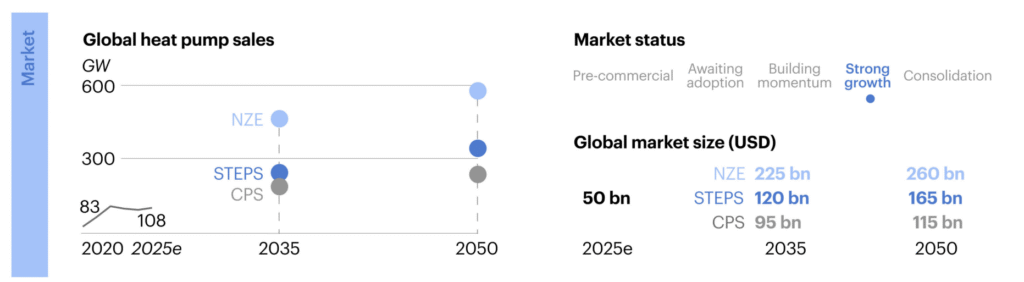

According to the report, global heat pump sales have more than doubled over the past decade, driven primarily by electrification policies, increasingly stringent energyefficiency standards, and growing energy security concerns. The report notes that in 2024 the global heat pump market reached an estimated value of around USD 50 billion, making it almost as large as the market for solar PV modules. China is identified as the leading market in terms of installed capacity, while the United States represents the largest market by value, accounting for more than USD 17 billion, or roughly one third of global sales. The report further highlights that Europe experienced particularly rapid growth following the energy crisis in 2022, although policy uncertainty and changes to subsidy schemes in 2023–2024 led to a temporary slowdown in several countries. Despite these shortterm fluctuations, the report concludes that heat pump deployment increases in all IEA scenarios, evaluated in the report, with heat pumps becoming a dominant heating technology in buildings by 2035, especially in advanced economies. Overall, the value of the market for heat pumps grows at around 2.5% annually to 2035 in the CPS and 6.5% annually in the STEPS.

“Heat pumps are gaining ground; lower electricity prices would push them even further”

Air conditioning

Space cooling is one of the fastestgrowing sources of electricity demand worldwide, which is conveyed by the IEA in this and several earlier reports. Since 2000 household AC ownership has tripled globally (to ~40%) and electricity use for cooling has already more than doubled. Market saturation is already high (70–90%) in the US, Japan and China, but future growth is concentrated in emerging economies, where rising incomes and hotter climates coincide, according to the IEA analysis. The report highlights that cooling demand growth is structurally locked in, even under strong climate policy scenarios.

Costcompetitiveness: operating costs improving, upfront costs still a barrier

Heat pumps for buildings

It is stated in the report that heat pumps are already the lowestcost heating option in several regions when operating costs are considered.

- Airtoair heat pumps are especially competitive in Mild climates

- Regions with high cooling demand

- Areas where electricity prices are favourable relative to gas

- In colder regions (e.g. Northern Europe, Canada), competitiveness depends strongly on:

- Electricitytogas price ratios

- Longterm policy certainty

The report concludes that upfront investment costs remain the main barrier, particularly where subsidy schemes are unstable or complex.

Industrial heat pumps

While heat pumps for buildings are a considered a mature technology, industrial heat pumps remain at an early commercial stage:

- Today they supply <5% of global industrial heat

- In the STEPS (stated policies) scenario they reach ~2% of lightindustry heat demand by 2035

- Capital costs are 3–10 times higher than fossil alternatives, making electricity pricing and policy support decisive.

Air conditioning

When it comes to air conditioning large efficiency gaps persist, according to IEA. Bestinclass units can be up to four times more efficient than the least efficient models still sold globally. According to IEA’s mapping, more than 100 countries now apply minimum energy performance standards (MEPS), covering ~90% of global cooling demand. However, highefficiency units remain more expensive upfront, slowing uptake in costsensitive markets despite lifecycle savings.

Manufacturing; present status and outlook

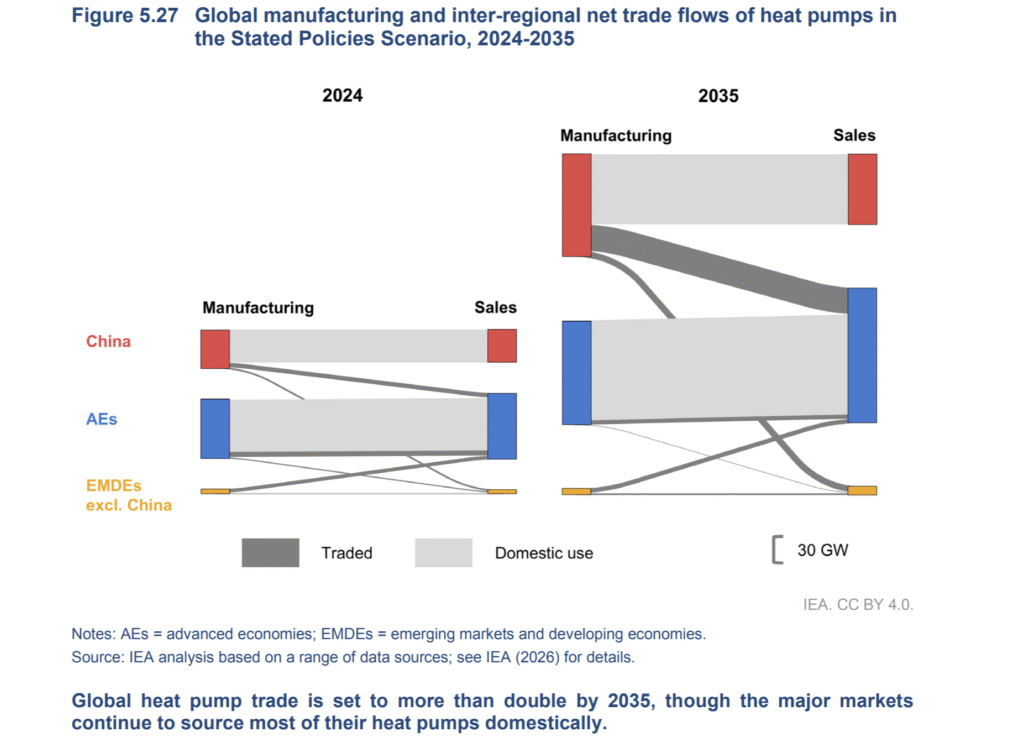

The report reveals that the manufacturing of heat pumps for building applications remains geographically diverse, though upstream segments such as component production are more concentrated. In 2024, only around 15% of heat pumps installed worldwide by capacity were traded across borders, with most demand met by domestic production. All major markets – China, the United States, Europe and Japan – sourced over 70% of their heat pump supply locally. Global manufacturing capacity is around 145 GW led by China (35%), followed by the United States (25%) and the European Union (20%).

Heat pump manufacturing is projected to grow sharply over the next decade. Key policy drivers include heat pump subsidies, building energy codes, carbon pricing, national heat plans and heat pump targets, as well as policies aimed at training and skills development. In the STEPS, capacity rises 80% in China, more than doubles in the United States and rises by about 40% in the European Union by 2035. By then, these three markets account for 85% of global manufacturing capacity and 80% of demand, cementing their central role in shaping the industry’s future, according to the report. Moreover, IEA’s analysis shows that the heat pump market grows even faster in the NZE (net zero emission) Scenario, with global sales more than quadrupling to 2035 on the back of far stronger policy measures than those currently in place.

Supply chains: concentration creates vulnerability

The analysis behind the report shows that there is a particularly acute supplychain risk for compressors. 90% of rotary compressor production is in China and on third of scroll compressors are produced there. Compressors account for up to onethird of total unit cost, making this concentration strategically important. The report explicitly flags compressors as a shared vulnerability across heat pumps and AC, with implications for energy security, trade disruptions and industrial policy design in Europe, the US and India.

Cost structure and industrial competitiveness

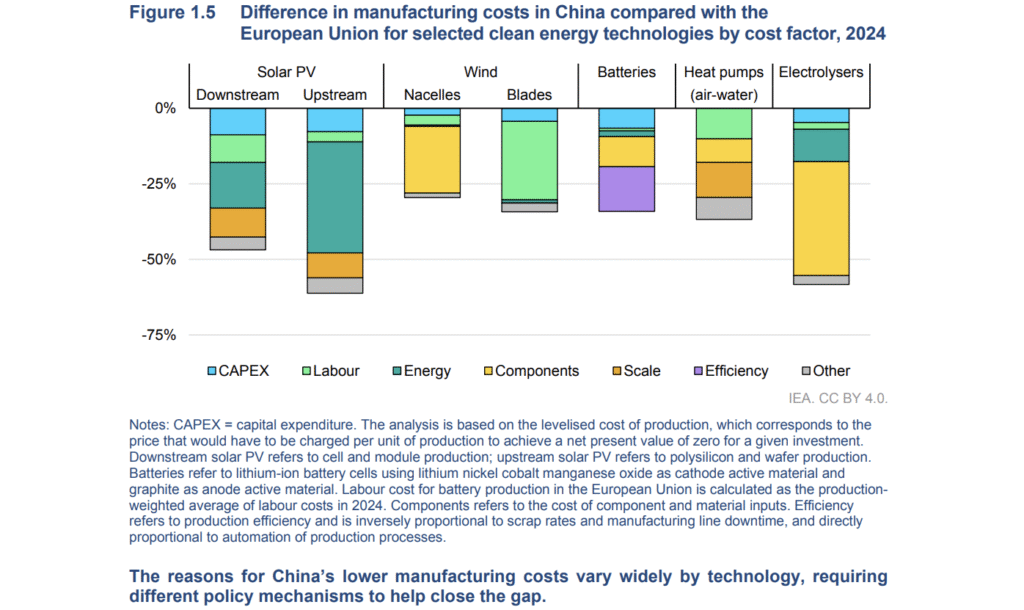

Manufacturing costs for heat pumps and air conditioning units are lowest in China, due to scale and automation, vertical integration and dense component supply chains. Compared with China, Japanese heat pump production costs are ~40% higher and European airtowater heat pumps can be ~60% more expensive, according to the mapping performed by IEA.

For heat pumps, the cost gap is driven primarily by:

- Labour cost

- Component costs (especially compressors)

- Production scale

- Integration across AC and heat pump product lines

The report stresses that industrial policy focused on scale, automation and component ecosystems is more effective than trying to compete on labour or energy costs. However, the implications of lower equipment prices in the total cost for installation is still relatively limited and it is therefore very important to also take measures to limit the rest of the cost (labour etc) related to the installation of the heat pump.

Cooling demand, electricity systems and flexibility

ETP 2026 underlines that cooling demand will increasingly shape electricity systems. Air conditioners is already a major driver of summer peak loads in many regions while heat pumps add winter peaks in colder climates. Without efficiency gains, cooling demand could significantly increase grid investment needs.

However, the report also highlights the flexibility potential:

- Smart heat pumps and air conditioner units can support demandside response

- Digital controls, thermal storage and dynamic tariffs improve system integration

These features are becoming standard in highend markets but remain underutilised elsewhere.

Policy messages highlighted in the report.

Across all scenarios, the ETP 2026 consistently points to the following priorities for heat pumps and air conditioners:

- Stable, longterm policy frameworks matter more than shortterm subsidy levels

- Adjust energy taxes and levies while encouraging flexible demand, including via targeted R&D support

- Avoid abrupt changes to incentives or regulations.

- Expand fast-track reskilling programmes and integrate heat pump training into vocational education

- Establish one-stop-shops for advice and installation, streamline permitting processes and encourage innovative business models (e.g. leasing).

- MEPS (minimum efficiency performance standards) for cooling are among the most effective and least costly climate policies

- Supplychain diversification for compressors and key components is a strategic priority for energy security, affordability and climate change mitigation

The Technology Collaboration Programme on Heat Pumping Technologies (HPT TCP) has contributed with facts to and review of the ETP 2026 report.

Source: https://www.iea.org/reports/energy-technology-perspectives-2026 International Energy Agency.