The International Energy Agency’s eleventh annual World Energy Investment report, released in June 2026, maps a global energy sector in which capital flows are expected to grow to USD 3.4 trillion in 2026, a 5% rise from 2025, with around USD 2.2 trillion directed collectively to renewables, nuclear, grids, storage, low-emissions fuels, efficiency and electrification (p. 6). The report is framed against the destabilising effect of the Middle East conflict and what the IEA calls the largest energy security threat in history, with roughly three-quarters of anticipated 2026 energy investments effectively locked in by earlier decisions (p. 6). For the heat pumping community, the central message is structural rather than cyclical: electricity-related spending already accounts for nearly 60% of all global energy investment, and electrification through heat pumps, electric vehicles and electrified industrial processes is expanding at around 15% year-on-year, even where it advances unevenly across regions (p. 9, p. 106). The report positions heat pumps not only as a decarbonisation lever but as an instrument of energy security and system resilience, alongside electric vehicles and electrified industrial heat (p. 132).

Europe leads the early-2026 rebound

The clearest near-term signal comes from Europe. According to the IEA (p. 9), available heat pump sales data for Europe show a 17% year-on-year increase in the first quarter of 2026, despite subsidy scale-backs in certain countries. The report presents this in its overview as the strongest growth among tracked electrification categories in Q1 2026, with the chart “Growth by category, Q1 2025-Q1 2026” placing European heat pump sales alongside EV sales across regions and a surge in induction cookstove sales in India (p. 21). The IEA notes that the European figure aggregates first-quarter sales across Austria, Belgium, Denmark, Finland, France, Germany, the Netherlands, Norway, Poland, Sweden and Switzerland, drawing on European Heat Pump Association data (p. 21).

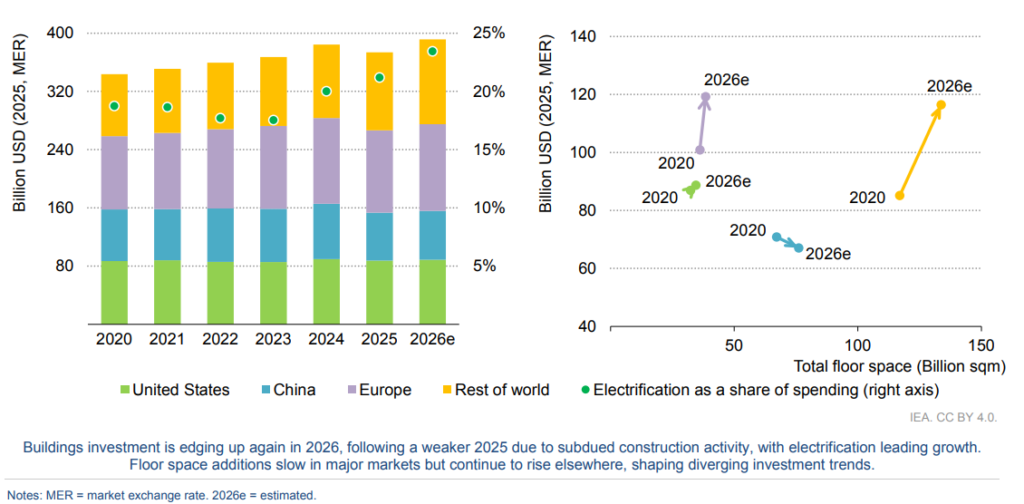

Buildings investment recovers and electrification gains share

This momentum sits within a broader buildings-sector recovery. After a weaker 2025 constrained by subdued construction activity, buildings investment is edging up again in 2026, with electrification leading the growth and gaining a larger share of total spending (p. 109). The demand fundamentals are strong: the report forecasts that buildings will account for half of global electricity demand growth through 2030, largely reflecting residential adoption of electric heating, cooling and appliances (p. 113). In the European Union specifically, an additional 300 TWh of electricity demand is forecast by 2030 from fairly broad-based growth across electric vehicles, heat pumps, cooling, industry and some data centres (p. 80).

Sales stabilise as the economics turn competitive

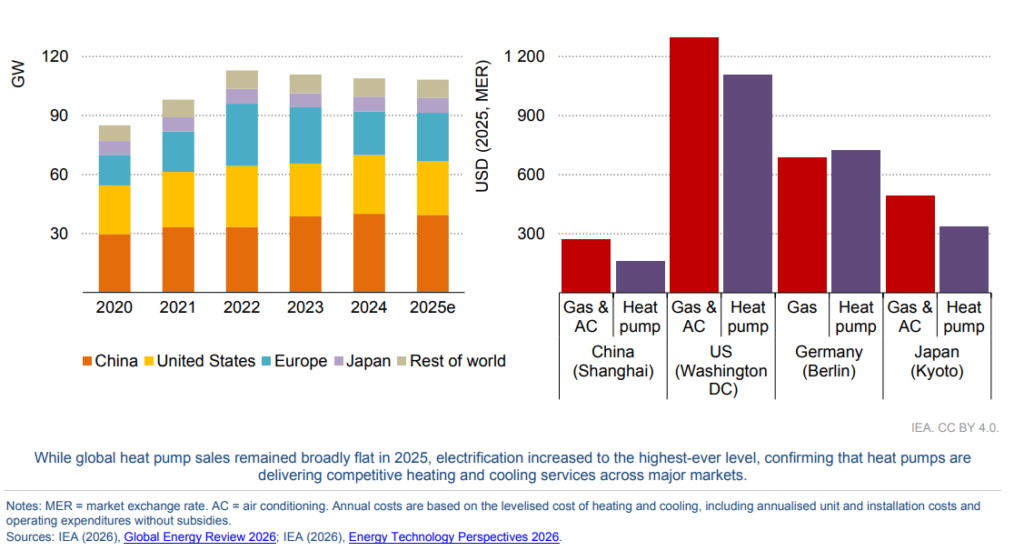

At the annual level, the picture is one of consolidation rather than contraction. The report states that while global heat pump sales remained broadly flat in 2025, electrification increased to the highest-ever level, confirming that heat pumps are delivering competitive heating and cooling services across major markets (p. 115). The supporting figure “Global heat pump sales, 2020-2025” charts sales in gigawatts across China, the United States, Europe, Japan and the rest of the world, paired with a comparison of estimated annual average residential heating and cooling costs for 2024 across Shanghai, Washington DC, Berlin and Kyoto on a levelised-cost basis without subsidies, drawing on the IEA’s Global Energy Review 2026 and Energy Technology Perspectives 2026 (p. 115). The IEA cautions, however, that household uptake remains tightly linked to relative fuel prices, with adoption slowing when electricity costs exceed roughly two times the price of gas, underscoring the role of taxation, subsidies and regulated pricing in investment decisions (p. 113).

Public finance remains the decisive variable

The report is explicit that buildings-sector electrification continues to rely heavily on public funding, particularly for projects with high upfront costs and long payback periods (p. 110). In the European Union, 2026 is described as a decisive year for the NextGenerationEU Recovery and Resilience Facility: of its EUR 577 billion in funds, only around 60% had been disbursed by early 2026, leaving roughly EUR 270 billion still to be allocated, and because at least 37% of spending must support climate objectives, much of the remaining funding is being directed towards building renovations, heat pump deployment and upgrades to social housing (p. 110). The household-level policy mix is captured in the figure “Demand-side affordability policies supporting household energy efficiency investments, 2025,” which breaks out heat pumps as a distinct technology category alongside retrofits, solar PV, efficient appliances and battery storage, mapped against instruments and regions (p. 113).

Asia-Pacific energy security sharpens support

Outside Europe, energy-security concerns are driving renewed public spending. The report records that net fossil fuel importers including Japan and Korea are scaling up programmes to reduce exposure to fuel price volatility (p. 111). In Korea, national and local governments have introduced additional subsidies to electrify heating and install heat pumps, plus a dedicated buildings-sector efficiency scheme for low-income households starting in 2026 (p. 111). In Japan, government-backed programmes continue to support deployment of high-efficiency heat pumps and advanced climate systems in line with the Strategic Energy Plan’s emphasis on electrifying heat (p. 111). The figure “Buildings-sector energy efficiency and electrification investments, and fossil fuel shares in space heating, 2015-2025” illustrates the declining fossil share in space heating alongside rising electrification investment (p. 111).

A note of caution from the United States

The report does not present a uniformly positive picture. In the United States, the IEA observes weakening demand for heating and cooling equipment, reflected in a sharp year-on-year drop in central air conditioner and heat pump sales, linked in part to the legislative changes of 2025 and the phasing out of some consumer-facing incentives (p. 110, p. 127). This divergence illustrates the report’s broader thesis that similar technologies can scale rapidly in one region while stagnating in another, depending on the alignment of infrastructure, prices and finance (p. 106).

Heat pumps in supply-side and manufacturing accounting

Beyond end-use demand, heat pumps appear in the report’s supply-side and manufacturing classifications. Large-scale heat pumps are grouped within the “Other clean power” category alongside fossil-fuelled power with CCUS, hydrogen and ammonia in the report’s fossil and clean power investment accounting (p. 225). In clean energy manufacturing, heat pumps are included within the “Other” technology grouping together with electrolysers and wind turbine components, a category set against an overall clean energy manufacturing investment that peaked at USD 227 billion in 2023 before declining amid solar PV overcapacity (p. 158).

Connecting to international collaboration

For readers tracking the technology development that underpins these market figures, the HPT TCP’s ongoing projects on industrial heat pumps, high-temperature applications, district heating integration and digitalisation provide the complementary technical and demonstration evidence base, accessible at https://heatpumpingtechnologies.org/ongoing-projects/. Read together, the investment data and the collaborative research programme describe the same transition from two vantage points: capital allocation on one side, and technology readiness on the other.

Outlook

The 2026 data suggest heat pumps have crossed from a subsidy-dependent growth phase into one where competitiveness, energy security and policy design jointly determine the pace of deployment. As the IEA’s record electrification share and Europe’s 17% first-quarter rebound indicate, the question for the next phase is no longer whether heat pumps work, but whether finance, grids and stable policy can scale them fast enough to meet the demand growth they are designed to serve.

Source: IEA (2026), World Energy Investment 2026. The full report can be accessed at https://www.iea.org/reports/world-energy-investment-2026.