Background to the Guidance Tool

This page provides more detailed information about the background and working of the “Smart Guide”: you can use the Guide without reading it.

60

Disclaimer

This tool has been developed within HPT TCP Project 60, and the project participants have verified the outputs of the tool. The outputs from the tool do not necessarily represent the views of the HPT TCP and its individual member countries.

Comments & Questions

This is version 1.0 of the tool. In case you have any comments regarding the functionality of, or outputs from, the tool, or if you have possibilities to complement the tool with more case studies, please contact the Heat Pump Centre and write “Project 60 System and Case Studies Smart Guide” in the topic field. Such information will be considered in a future possible revision of the tool.

How the Guide works

Who is the Guide for?

The purpose of the guidance is to help decision-makers within organizations that own or occupy non-domestic buildings to prepare themselves for detailed discussions with suppliers, installers, and designers of retrofit heat pump systems.

It is likely to be most useful to those who have not previously procured heat pumps for existing buildings and those who do not already have easy access to designers or installers who are familiar with such projects.

It only provides initial outline guidance as a preparation for more detailed discussions with experienced installers and designers who have inspected the building. They are likely to ask the same questions that the guidance tool poses and should be able to help to provide the answers based on what they have seen and on your records of energy use.

Fitting a heat pump should be considered alongside the possibility of taking other measures to reduce energy use and carbon emissions which the guidance tool does not consider. These could include changes to the operation of the heating system, improvements to the building fabric or the provision of other low-carbon technologies such as solar panels. Experienced advisors should be able to advise you on these measures.

This suggests that early-stage guidance such as the on-line the “Smart Guide” will be most useful to small and medium- sized businesses who have responsibility for their own heating; to professional engineers in their early discussions with clients; and

The guidance should also be helpful to inexpert decision makers within other types of enterprise including members of the financial approval chain in larger organizations

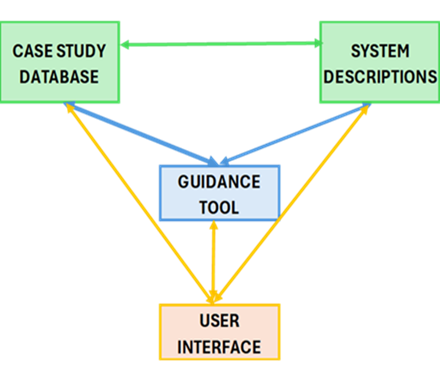

Overview of the Tool

The smart guide has four main components, with potentially six two-way links between them: a database of existing nondomestic heat pump retrofit “case studies”; a list of 30 possible systems, with summary and more detailed descriptions of them; a user interface; and the “smart guidel” logic.

The user interface allows the user to either directly access the “case study” database of information sheets on existing heat pump retrofits, or the system descriptions, or to use the “smart guide” to create a bespoke shortlist of system options based on responses to 14 questions. The “smart guide” then selects those case studies that use one of the shortlisted systems and also most resemble the characteristics defined by the user.

This approach is similar in principle to the initial design stage commonly used by system designers, of identifying several apparently feasible initial options for more detailed analysis. Although it was developed independently, it is also very similar to the decision flow process previously developed by the Energy Systems Catapult in the UK who subsequently became a participant in the project.

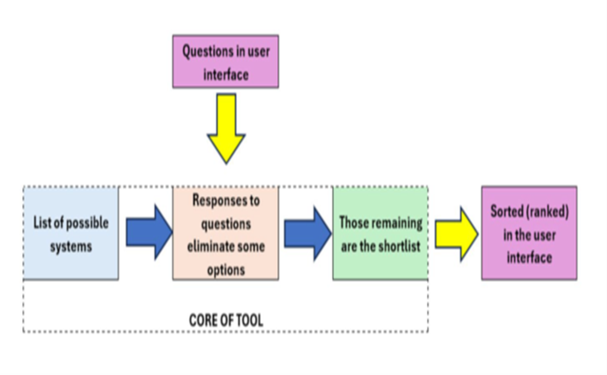

How does it create the shortlist?

The creation of the shortlist is a filtering process which removes options from the original list of possible systems according to the responses to the 14 questions. The potential number of possible system configurations is impractically large to consider every one at this level of guidance – it is at least 200: the 30 that are included were selected to include the range of practical possibilities in the participating countries.

The heating systems can be classified into several overlapping groups, air to water systems, hybrid systems, ground or aquifer to water systems, surface water to water systems, heat recovery options, systems that can provide cooling, and single-room options. These are described under “overview of systems”

A list of the different heating systems and their characteristics and the a list of the filtering questions can be found in Appendixes to the project final report.

How does it select example installations?

Initially, the database of example installations (“case studies”) contains about 50 installations, mostly from the UK but including examples from all countries participating in the project. Many more have been obtained and more will be welcome, especially if they describe situations that are not currently covered, or include “as measured” performance or costs.

The key features of each example are identified in the database, allowing the tool to search for those of most relevance to a particular enquiry. In deceasing order of priority, the criteria are;

• The new system type is on the shortlist

• The original HVAC system matches that entered by the user

• The level of change to the building fabric or the HVAC system study matches the expected level entered by the user

• The building type matches that entered by the user

• The floor area class matches that entered by the user

Case Study Statistics

General

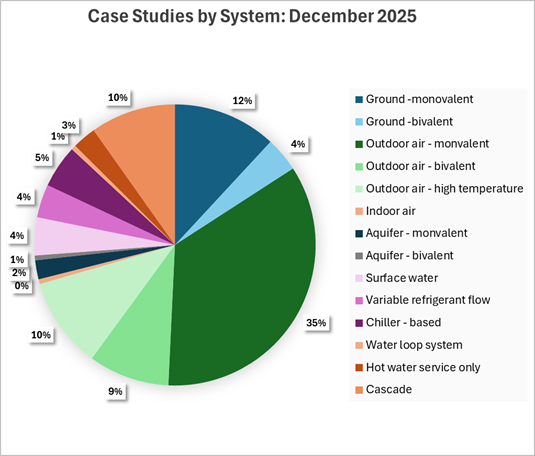

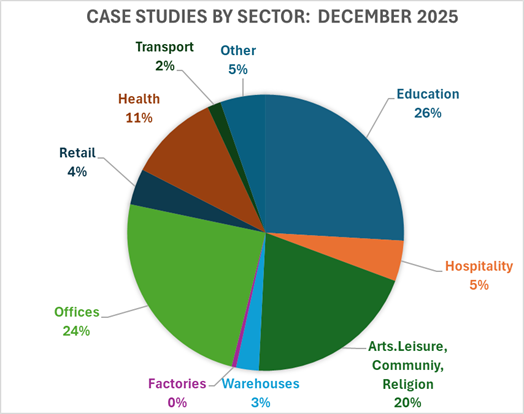

As of the end of the project at the end of 2025, nearly 200 examples of retrofit case studies had been identified, predominantly from the UK, These are summarized in the sections below. While these can offer a (largely UK-biased) insight into the current market, they do not come from a structured survey and cannot be considered to provide an accurate detailed picture. Many of the retrofits are sourced from websites or technical journals and are presumably produced to illustrate the skills of system designers and installers or the environmental credentials of building owners of occupiers. Some specific caveats are mentioned in the relevant summaries.The percentages shown in the diagram are by number of buildings and will under-represent sectors where a reported refurbishment project applies several buildings on a common campus: such as hospital sites.

Types of System

The potential size of the non-domestic market is uncertain but is certainly much smaller by number than that for dwellings: the UK market penetration rate appears to be about half that for dwellings.

Examples of heat pump retrofits can be found in all nondomestic market sectors, but are most numerous in the Education, Arts Leisure and Community, Health, and Office sectors. The first three of these sectors are predominantly publicly-owned buildings and the number of examples is also relatively high compared to the number of public sector buildings in the stock. This is presumably a reflection of the existence of theUK Public Sector Decarbonisation Scheme (PSDS) which provided financial support to projects that met the scheme’s requirements in the years preceding the project. Although not specifically targeted at heat pump retrofits, in practice most of the projects did include heat pumps.

The office sector mostly consists of private-sector buildings, though it does contain some that are in the public sector. A common trigger for refurbishment in offoces is the opportunity to increase the rental value of a well-sited office by – amongst other measures – upgrading its energy and environmental credentials. This requires the existence of potential tenants who value these features, for example because it pre-empts upgrades to meet future level of minimum energy efficiency regulations.

Some other sectors, such as hotel or supermarket chains, may be under-represented because their owners or tenants prefer to showcase their environmental credentials at a corporate level rather than building by building.

Case Study Statistics: Market Sector

The majority of retrofit systems are based on air to water heat pumps, of which an uncertain proportion avoid the need to possibly replace heat emitters either by using “high temperature” heat pumps or by being hybrid systems (reports are often unclear). Ground-source systems are typically larger than air-source systems, so their importance in energy terms is under-represented.

About 10% of systems provided active cooling (some ground source heating systems can also provide passive cooling and can recover heat rejected from cooling as a source of heating when there is a simultaneous need for both services. In some cases cooling was added an element in upgrading an existing heated-only building. It is probable that the routine installation of reversible room air conditioners or VRF systems would be less likely to be seen as meriting specific publicity and are under-represented.

The term “cascade system” is somewhat ambiguous but generally taken to mean a system where separate heat pump is used to increase the water temperature provided for space heating to a level suitable for the provision of a hot water service: and is sometimes reported as an “air -source plus water source” system.

Building Size

The example projects were classified by heated floor area: small (<1000 m2); medium (1000 to 5000 m2) and large (>5000 m2). 10% of the projects that reported floor area were “small”; 48% “medium” and 42% were “large”. These categories account for approximately 95%, 5% and 1% of UK non-domestic buildings) so the implicit market penetration rate is very much higher for larger buildings.

Level of Refurbishment

The example projects were also classified by the “level of refurbishment of building fabric or system”: low; medium; high.

”Low” was intended to include replacement with little if any modification to the heating system or the building, and ”high” to ”deep” buildng renovation or complete replacement of the heating system. Where it was reported, the installation of other carbon abatement measures was treated as a refurbishment activity.

It is not possible to be definitive but it appears likely that about one fifth of reported retrofits were triggered or facilitated by a need for extensive building or heating system refurbishment, nearly half were retrofits accompanied by a minimum of other changes (so, in some sense the buildings were “heat pump ready”) and, in the remainder, other measures were taken either to enable heat pump retrofit, to further reduce carbon emissions or because it was convenient to renovate the building as part of a wider refurbishment project. (The proportions may have been influenced bythe UK PSDS requirements which encourage a whole-building approach to decarbonisation).

This illustrates the need for policy makers and suppliers of heat pump retrofit system to consider heat pump retrofit as one component of a broader approach to decarbonisation, and that system designers and installers should be being competent to advise on these wider issues.

Overview of Systems

Introduction

This page provides more detailed information about the background and working of the “Smart Guide”: you can use the Guide without reading it.

The following paragraphs provide an overview of the principal categories of heat pump systems. Longer descriptions of each system and a mapping of particular systems against these categories can be found in the Project final report.

Air-to-water systems

These systems generally have lower upfront cost than other systems. Standard heat pumps may require radiator upgrades, or the replacement of heating coils in air handling units, but high-temperature heat pumps or hybrid systems can avoid this. Care is needed with pipework design and controls when replacing boilers. Rooftop mounting is common for larger systems. Generally quiet but this needs checking for local sensitivities. Special heat pumps are available for use in cold climates.

Ground- or Aquifer–Water Systems

This category includes two types of system: those that extract heat from underground water sources, and those extract heat from the ground itself – more information on the differences between them can be fond in the Project final report”. Aquifer systems and larger ground source systems use vertical boreholes to reach the aquifer or for heat exchange with the ground. Suitable locations for drilling are therefore needed.. In new buildings the heat exchangers may be integrated into the structural piles, but this not usually possible for retrofits. For smaller systems, horizontal heat exchangers may be installed in shallow trenches. These systems are relatively expensive due to drilling costs and the need for surveys if the geology or hydrogeology are uncertain. Extraction and return of water will require environmental permits. In summer, heat from air conditioning may be rejected into the ground, providing an element of inter-seasonal heat storage. Efficiency is high and insensitive to the air temperature, which makes the systems suitable for use in cold climates. The combination of high efficiency but high cost can make ground source heat pumps financially attractive as the “base load” element of a monovalent hybrid system (with a lower-cost, less efficient top up element)

Other Water-water systems

Extracting heat from surface water can provide high efficiency provided that the body of water used is of sufficient size and depth to act as a seasonal thermal reservoir (when considering ponds or lakes) or to have enough water flow (when considering rivers) so that the heat and water drawn from them do not have negative impacts on the thermal stratification of the water body or its ecological environment. For these reasons, environmental permits will be needed. While the direct use of the extracted water is possible, the use of heat exchangers and a separate system circuit is more common. Reversible systems, able to produce either chilled water or heating water, are possible depending on the water body being considered.

Heat Recovery Options

Waste heat that is warmer than outdoor air is an attractive heat source for high efficiency heat pump heating systems if it is reliably available during the heating season. Heat pumps are well-suited to heat recovery from high-humidity spaces such as swimming pools because they can cool the exhaust air below its dewpoint and recover latent heat. Sources of waste heat such as sewage or industrial waste heat require careful system integration that is more easily incorporated into new-build or major refurbishment projects unless low-carbon heat is available from a nearby heat network. Some types of air conditioning system lend themselves to heat recovery: for more information on these see the notes on systems that can provide air conditioning.

Hybrid (bivalent) Systems

Bivalent hybrid (air, ground or water source) systems combine electric heat pumps and fossil fuel heat generators, They avoid the need to upgrade heat distribution systems and have lower peak electricity demands. They generally have relatively lower initial costs but provide lower carbon abatement and can be an initial step towards deeper carbon abatement when future fabric improvements are planned. Systems that combine different types of heat pump, such as ground- and air-source heat pumps: ”monovalent heat pump systems” are sometimes described as ”hybrid” but within this report the term is reserved for bivalent systems unless stated otherwise.

Systems that can provide cooling

There are several ways of using heat pumps with existing air-conditioning systems. If the existing heating system has a fossil-fuelled water-based distribution system – typically using a boiler – the heat generator can be replaced by air- ground- or water- source heat pumps of the types described above. Ground-source systems provide a degree of inter-seasonal heat recovery by warming the ground in summer and cooling it in winter. The heating function can also be provided by reversible versions of chillers, room air conditioning units or rooftop units. For air-based air conditioning systems, integrated heat pump / air handling units can be installed.

Where there are simultaneous heating and cooling demands, it is possible to recover the heat rejected by the cooling system to satisfy part of the heating demand, thereby increasing system efficiency. This can be done using a “multivalent” chiller or by installing a decentralised type of air conditioning system, such as water-loop heat pumps or variable refrigerant flow (VRF). As its name suggests, a water-loop system links several reversible heat pumps together by a common water circuit with each unit, each of which extracts heat from or supplies heat to the circuit according to whether it is in heating or cooling mode. The remaining need for heating or cooling is provided centrally to the water circuit by central units. VRF systems achieve the same result by linking individual room units by refrigerant circuits. Some VRF systems now use water for the indoor circuits in order to comply with regulatory constraints for refrigerants.

The impact and viability of heat recovery depends on the annual duration of coincident heating and cooling demands, which is climate and building dependent. Suitable situations include buildings and climates where interior zones have cooling loads while perimeter areas require heating, or where different facades require heating and cooling at the same time.

Single-room Options

In most cases, the most appropriate single-room retrofit heat pump system is a reversible air to air room air conditioning unit. These are relatively low cost and have high efficiencies. Similar functionality for several rooms can be provided by VRF or water-loop heat pump systems (described in the “systems that can provide cooling” section).

Options for Hot Water Systems

In many nondomestic buildings, the space heating system is integrated with the provision of stored hot water for taps, showers and other appliances. Hot water needs to be stored at sufficiently high temperature to reduce the risk of legionella and other bacteria, which may require the use of temperatures above those normally required for space heating. High temperature and hybrid heat pump systems can provide these temperatures and can replace a fossil-fuelled heat generator. The efficiency of the heat pump will be reduced at the higher flow temperatures and it is normal practice to reduce them at other times. It can also be provided by using a second heat pump to raise the temperature of a sub-circuit from that provided for space heating: this is known as a cascade system.

Generic Comparisons

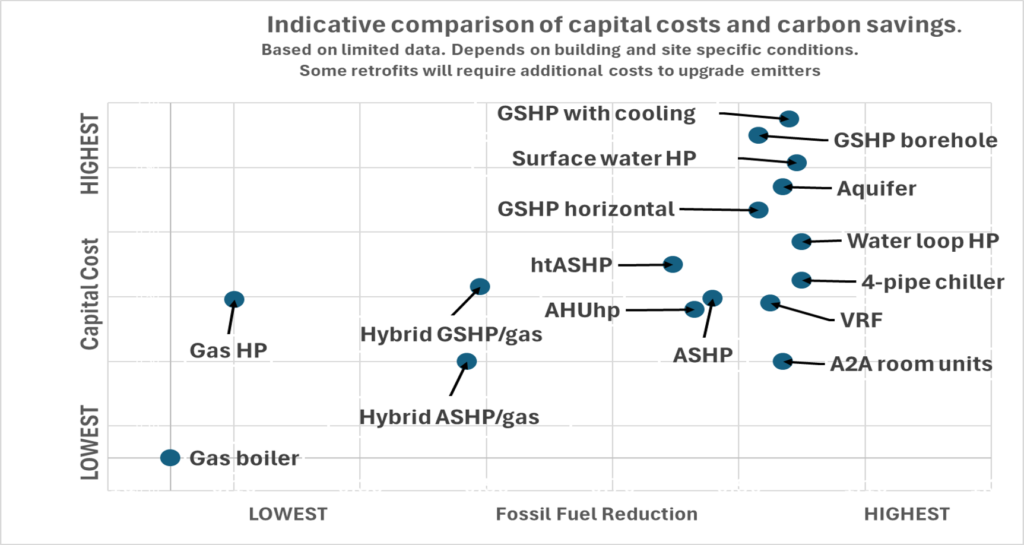

The relative performance and cost of different systems depends on specific characteristics of buildings, existing HVAC systems and the local climate. This comparison chart can only provide very broad generic guidance of the relative capital costs and the carbon savings when heat pumps a replace fossil-fuelled heating system

The vertical scale shows a relative capital cost index and the horizontal scale a relative index of reduction in fossil fuel (and therefore carbon) savings.The scales areconstructed so that the best-performang system has a rating of 1, and the perfomance ofther systems is expressed as a fraction of this. As a result, the indices are insensitive to changes in absolute prices (though relative costs for different systems may change with time and location) or to the carbon intensity of the electricity supply. (A more detailed explanation is provided in theproject final report). Because of the factors described above, each point on the chart should be understood as being an approximate indication, surrounded by a cloud of uncertainy. Detailed assessments should be made for specific projects using project-specific information.

Systems with the low capital costs and high carbon savings are located in the bottom right hand section of the chart. (If the price of low-carbon electricity is below that of fossil fuel, this will equate to a shorter financial payback).

National Perspectives

Overview of the UK market

In addition to contribution to the development of the ”Smart Guide”, some participants provided information and insights from national studies. Although each market inevitably reflects the impact of the national building stock, ownership profile and the policy measures that are in place or expected, these national perspectivss have relevance to markets and policies generally.

Although the project did not explicitly address market or policy issues, it did obtain some relevant information in the course of locating case studies and other interactions with participants in the market. Each market inevitably reflects the impact of the national building stock, ownership profile and the policy measures that are in place or expected. This section presents a general perspective of the current and potential UK non-domestic heat pump retrofit market, in particular approximate indicators of the scale of impact of conceivable regulatory measures. It relates specifically to the UK but is believed to also have broader relevance. Data are sparse and of sometime uncertain reliability so the numbers should be viewed as indicators of relative magnitude rather than rigorous estimates. In some cases the estimates are based on AI inferences but checked for plausibility against relevant primary sources where possible.

Current Situation

The current UK stock of nondomestic buildings is about 2 million, accounting for about one third of the of heated floor area in buildings, which are of widely differing sizes and uses. Slightly fewer than 50% are leased to tenants. It is thought that the there are about 300,000 public buildings. About 15,000 new non-domestic buildings are constructed annually. About 75% of the existing buildings have fossil-fuelled heating. About 40% are believed to have some form of air‑conditioning: the heating service in chiller-based systems is normally provided by fossil-fuelled boilers, but single- and multi-space air to air systems are commonly reversible and able to provide heat pump heating, in some cases using rejected heat from the cooling service.

The annual number of non-domestic heat pump retrofits is estimated to be about 2000 to 3000. The 250 or so public sector projects per year supported by PSDS represent an above-average (but still low) level of market penetration.

Triggers, motivations and barriers

The “triggers” for considering a heat pump retrofit are:

- The actual or expected breakdown of a fossil-fuelled heat generator.: typically about 7% of the heat generator stock each year, say 10,000 per year.

- The replacement of heat distribution system because of change of building use or system deterioration: perhaps about 3% of the stock per year, say 4,000 per year. This is likely to be accompanied by replacement of the heat generator. To avoid double-counting the number of leaving heat generator-only triggers is reduced to 6,000.

- Major refurbishment of a building because of expected of increase rental or building value, , building change of use or deterioration to: say 1% of the stock per year or about 1,000 per year (roughly equivalent to the new-build rate). If this includes system replacement, to avoid double counting, the overall figures become

- (Fossil fuelled) heat generator only: 5,000

- Heat distribution system renovation or replacement including heat generator replacement: 3,000

- Major building renovation including system and heat generator replacement: 1000

This list does not explicitly include the trigger provided by the 1,000 or so replacement air conditioning chillers installed each year. This will not always coincide with the need to replace the heat generator, but offers an opportunity to replace cooling-only chillers with “polyvalent” heating and cooling chillers that can wholly or partially replace fossil fuelled heat generators. The installation of new air reversible room air conditioners and VRF systems in existing buildings. Numbers are uncertain but annual sales of room air conditioners are typically around 200,000 per year, of which perhaps half are like-for-like replacements, a quarter new installations in existing buildings and the remainder in new buildings. The like-for-like replacements will only affect carbon emissions to the extent that they are more efficient than the units that they replace – most units are already reversible – but the new installations in existing buildings have the potential to replace fossil-fuelled heating. Sales of VRF multi-room systems are much lower but fewer will be like-for-like replacements and they can be particularly suitable for new installation in existing buildings so probably account for several thousand systems per year. Many of them can recover heat rejected from cooling some rooms for use in heating others, in which case the carbon efficiency is high.

The motivations to choose a heat pump option will differ between purchasers but is likely to be a mixture of meeting regulatory requirements, expected financial benefits and environmental concern. The main barriers are: higher capital and operating costs, concern about the performance of an unfamiliar and relatively untried new technology, and the related difficulty of identifying competent, experienced installers. Heat pumps are not the only means of satisfying the objectives and are often associated with other carbon-reduction activities such as operational changes, improvements to the building fabric or HVAC system, more efficient lighting or the installation of photovoltaic panels. This blurs the distinction between the triggers listed above and also means designers and installers of retrofit heat pump systems should have additional competencies than the ability to design and install effective and reliable heat pump systems.

Potential impacts

Several possible regulatory policies that would impact on heat pump uptake have been voiced and it is instructive to look hypothetically at their potential impacts. In all the examples, the impact of exclusions – which would probably be needed – are ignored.

New energy requirements for new buildings are expected to set performance levels that would encourage the use of heat pumps. These would clearly impact the 15000 or so new buildings constructed annually, and probably the similar number of major building refurbishments.

Ban on new fossil fuel heat generators would convert the 10,000 per year heat generator replacement “triggers” to installations (ignoring the effect of life-extension measures). This would take about 15 years to decarbonise the stock – a similar timescale to that seen for the introduction of gas condensing boilers (or the market penetration of gas central heating)

Minimum Energy Efficiency Standards for privately rented buildings are currently set at an EPC rating of E but are projected to increase to D and the C. About 55% of the commercial stock is subject these requirements and the E to D and D to C bands each account for about 30% of the stock. Combined with an average lease duration of 7 years, translates into about 6000 upgrades per year for 7 years for each change. Many, but not all, of these are likely to include the installation of a heat pump (and there some buildings will be exempt.

Potential markets, guidance and stakeholder views in Austria

The Austrian Institute of Technology and the Austrian Energy Agency assessed the size of the technically feasible potential markets for heat pump retrofits in five categories of non-domestic buildings in the federal state of Salzburg by analysing over 5,600 energy performance certificates. This was supported by the development of generic guidance for each of the five sub-sectors: industrial and commercial buildings, hospitals, shopping centres, museums and educational institutions, linked to discussion of several case study buildings. The full report on this study: IEA HPT ANNEX 60 GUIDE Potential analysis for heat pump solutions in non-residential buildings” can be found on the Project website [to be confirmed]

In addition, Austria was the only participating country that carried out a systematic study of stakeholder views (reported below)

Technically feasible potential markets for heat pump retrofits

The energy performance certificates were filtered to remove types of building that were outside the scope of the study, They were then sorted by building use, floor area, thermal building standard, and the provision of three categories of thermal building services: room air conditioning, heat supply and hot water production. It was not possible to identify the magnitude of the heating and cooling requirements or the availability of outdoor space from the certificates. Buildings that used district heating or biomass were discarded as being poor targets for heat pump retrofit.

| Percentage of buildings theoretically suitable for heat pump retrofit for specific services | ||||

| Building Service | Industry | Hospital | Shopping Centre | Education (including Museums) |

| Conditioning of supply air | 2% | 70% | 29% | 16% |

| Space heating | 30% | 20% | 37% | 20% |

| Hot water supply | 24% | 90% | 40% | 57% |

These figures should be seen the context that 26% of industrial buildings used district heating or biomass (other sectors had smaller percentages), 95% had natural ventilation, only 24% had a centralised hot water supply system and 3% already had a heat pump.

In hospitals 90% had a centralised hot water system, 30% had natural ventilation and 10% already had a heat pump.

In shopping centres, 20% had heat pumps, 60% used natural ventilation and 40% had centralised hot water systems.

In the education sector 10% had heat pumps, 60% used natural ventilation and 57% had centralised hot water systems8

Overview of Stakeholder Interviews

Structured telephone interviews were conducted with target stakeholders in telephone calls and online meetings. The interviewees included manufacturers and suppliers of heat pump systems, engineering design offices, and operators of heat pump systems in large non-residential buildings, including those of some of the case study buildings in the guidance tool database. They covered reference projects in office buildings, warehouses, production halls, hospitals, kindergartens, theatres and sports facilities. A general discussion was also held on the market penetration of heat pump systems in this building segment, the obstacles and difficulties encountered and how these could be overcome.

Current market development, Decision criteria for heat pumps. The interviews revealed that there is currently a high demand for heat pump systems in large non-residential buildings, with many enquiries from the industrial and commercial sectors in recent years. Many successful reference projects have been installed already. The main decision criteria in favour of heat pump systems over other types of heat supply in non-residential buildings include both policy and technical aspects. Independence from fossil fuels and marketing strategies, e.g. by presenting certain certifications for sustainable heating of buildings, were mentioned. However, the industrial advantage of simultaneous heating and cooling of production machinery and ventilation systems also seems to play a role in the decision-making process.

Barriers – General, Technical, Financial. The main barriers to the uptake of heat pumps identified by respondents are general challenges such as a lack of awareness among end users and building owners about the feasibility, applications and cost-effectiveness of heat pump systems through reduced operating costs.

There also appears to be a lack of knowledge among installers, e.g. about the importance of hydraulic balancing, the possibility of cascade connection of heat pumps for higher flow temperatures, etc. Another problem seems to be the shortage of qualified personnel and the overloading of the supplying companies, resulting in long delivery times.

Technical barriers to the installation of heat pump systems in large non-domestic buildings are mostly the frequent need for significant building renovation, space constraints and noise emissions for air source heat pumps, with soundproofing measures being often very costly. The limited performance range of currently available air source heat pumps, e.g. for high hot water demand, was also mentioned as a technical constraint in some cases.

Financial and regulatory barriers include the above-mentioned retrofitting of existing buildings, which is often costly and not anticipated by customers. Another problem is the separation of investment and running costs and the resulting lack of financial incentives for building owners.

There appears to be little or no investment support for building owners. Permits for groundwater and geothermal use, and the drilling required to obtain them, are also often a barrier to the choice of heat pump systems. Other challenges include heritage protection and high safety requirements for refrigerants in engine rooms, which are often not met in existing buildings.

Measures to increase market penetration. To increase market penetration of heat pump systems in non-residential buildings, our interviewees recommended focusing on building know-how, for example by communicating best practice examples and expanding the existing consultancy services. It was also suggested to focus on in-depth training opportunities, such as expanding training and education programmes, organizing in-depth workshops for design and installation personnel, or even subsidizing the educational costs in this sector.

Investment incentives for building owners (e.g. through tax rebates/deductibility) or expansion of the subsidy framework were also suggested by our interviewees. In the case of rental, the possibility of a warm rent system was mentioned as a suitable measure, so that investors also benefit from lower operating costs. Another option could be stronger regulation in the industrial sector, for example a mandatory requirement to use renewable heat for processes up to 130°C (like in the food/beverage industry).

Other European Countries

Little information was discovered during the project that specifically refers to non-domestic heat pump retrofit markets in other European countries. For example, the “Heat Pumps in the European Union – 2025 Status Report on Technology Development, Trends, Value Chains and Market” report [6] explains that ”The European Commission is continuously working to support the uptake of heat pumps in residential and industrial sectors” but does not mention the nondomestic buildings sector. The revised European Energy Performance of Buildings Directive (EPBD-IV) stipulates that each EU Member State must draw up a national plan for the renovation of buildings by the end of 2026. These must cover both residential and non residential buildings may provide more insight.[ref] [7]

In the Netherlands the total amount of space in commercial buildings to be climatised more sustainably is similar to that of dwellings although the rate of heat pump installations is lower, reflecting the different dynamics and market instruments of the two markets. Indoor climate control systems for commercial buildings are, for example, more bespoke than for dwellings.

There are several financial incentives aimed at stimulating owners, plus legally required reporting of a commercial building’s energy performance, and mandatory implementation of measures having a payback time of less than 5 years, to encourage renovations. 93% of installed heat pumps are in dwellings, but about one-third of installations are now in commercial domestic buildings: the proportion that are retrofits is unreported. In the year 2024, 50,000 heat pumps were installed in the 1.2 million commercial buildings. This is considerably more than the estimated sales in the UK, and in a much smaller market. [8]

AI searches produced apparently plausible but unverified perspectives for several other countries, although it is not clear that the information always distinguishes clearly Many between domestic and non-domestic markets. (AI searches on this topic lead back to Project 60)

| Country/cluster | Retrofit market maturity [not specifically nondomestic] | Main non‑domestic drivers | Main constraints |

| Nordics (SE, FI, DK, NO) | Very high | High energy prices, strong public‑sector programmes, district heating integration | Grid capacity, limited “easy” stock left |

| Germany | High, accelerating | 65% RES rule, KfW finance, municipal heat planning | Policy volatility, electricity–gas price ratio |

| France | Medium–high | MaPrimeRénov’, carbon tax on fuels, tertiaire decree | Legacy building stock, skills bottlenecks |

| Netherlands | High in some segments | Gas phase‑out, all‑electric newbuild, city heat plans | Network constraints, space limits for outdoor units |

| Italy | Medium, very incentive‑driven | Superbonus legacy, cooling‑led commercial demand | Stop‑go incentives, fragmented small‑building stock |

| Spain & Portugal | Medium, fast in service sector | Cooling demand, hotel & retail retrofits, EU funds | Lower winter heat load, split incentives |

| UK & Ireland | Medium, uneven | Public‑sector decarb, BUS, local authority schemes | Weak carbon price signal on gas, capex aversion |

Non-domestic low-carbon retrofit information from Canada

Canada was able to provide such data from design studies that evaluated the expected cost and performance of alternative solutions for the same buildings. This majority of this note is based on “Analysis from CNS” note provided by NRCan for Annex 60. A second section provides additional information and context from the “Decarbonising Canada’s Large Buildings” study by the Canadian Green building Council (CaGBC).

The CNS note is based on studies in which the Government of Canada hired various consultants to execute “carbon neutral studies” on selected federal buildings, with the purpose of providing “packages” of options achieving various level of energy and GHG reduction levels, up to 100% GHG reduction, optimizing as well for cost-effectiveness, with one packaged identified as “best option”. The general approach taken by the consultants has similarities to that taken in this project: a range of Energy Conservation Measures (ECMs) for each building was first identified (equivalent to the options filtering in the Smart Guidance tool) and the more promising were selected for further examination by energy modeling and the calculation of LCCAs. These ECMs were then recombined in various ways to prepare packages for the calculation of energy saving, GHG abatement and cost-effectiveness values. In a few cases, the increase in peak electricity demand was also recorded. The data in the NRCan note relates to a subset of the study results, comprising heat pump retrofits using various technologies, including some that include conversion of distribution systems for low temperature operation. They are not necessarily the “best practice” options for each building, which may have been ECMs without heat pumps.

The CaGBC study used whole-building energy modelling to evaluate the cost-effectiveness of deep renovation and retrofit opportunities across 50 different building archetypes and locations, reflecting a representative range of building types, size, age, and location. The reported results cover office, multi-unit residential buildings (MURBs), and primary school and laboratory archetypes that collectively constitute a large portion of Canada’s existing buildings and associated emissions. The deep renovation packages were rarely cost-effective under mainstream conventions, often resulting in a positive IRR which was below the cost of capital.

Descriptive Analysis of CNS data

The CNS study provides estimates of the cost and performance of systems for 18 buildings in different areas of Canada, focusing on data required to calculate the 25-year NPV (presumably with current carbon intensities for electricity supply). The range of options considered differed between buildings and the scope and presentation scope of the results took different forms. In total nearly 90 building/system options were assessed. In the analysis summarised below, the CAPEX per unit of carbon abated has also been calculated: NPV may be more important to policy-makers but the CAPEX of abatement is probably more salient to investors, especially if a carbon tax is applied. (Subsequently Canadian carbon tax rate has been increased and a 40-year period adopted for NV)

It proved very difficult to extract coherent results from the detailed information, even when the reported carbon savings were corrected for local carbon intensities of electricity.. Examination of the results from the perspective of the frequency of the “best” estimated cost or performance metric for each building reveals the characteristics summarised in the tables below. One consequence of this approach is that systems that perform reasonably from several perspectives but do not excel in any are hidden from view: relative rankings would be more satisfactory if they can be extracted.

It should be borne in mind that this analysis is based on a small number of federal, mostly air-conditioned office buildings and assessments that are sometimes difficult to reconcile with each other. As a result, caution needs to be exercised when applying the contents elsewhere. Nevertheless it seems probable that overall ranking lists can be developed for each characteristic, though this has not yet been done. It must also be noted that buildings located in different provinces may have vastly different emission factors for the local electric grid. Construction costs were also local for the building site, and time period when the study was performed (between 2018 and 2022).

| Numbers | By building | ||||||

| System type | Cases analysed | Cases rejected | Cases with positive NPV | With best NPV (which may be -ve) | With lowest CAPEX | With highest carbon savings | With lowest Capex per kgC saving |

| Bivalent GSHP (covers a wide range of levels) | 18 | 0 | 28 | 8 | 2 | 11 | 7 |

| WSHP | 2 | 2 | 1 | 0 | 0 | 0 | |

| ASHP | 2 | 3 | 0 | 2 | 2 | 2 | 3 |

| Distributed heat pumps (WLHP) | 19 | 3 | 9 | 3 | 6 | 2 | 5 |

| VRF | 6 | 2 | 6 | 0 | 0 | 2 | 0 |

| Heat Recovery chiller | 7 | 0 | 0 | 2 | 3 | 1 | 3 |

| Non HP measure | 2 | 2 | 1 | 1 | 2 | ||

Table 1 By number of cases

| Percentage of cases | Percentage of buildings in which option was considered | ||||||

| System type | Cases | Rejected | With positive NPV | With best NPV (which may be -ve) | With lowest CAPEX | With highest carbon savings | With lowest Capex per kgC saving |

| Bivalent GSHP (covers a wide range of levels) | 20% | 0% | 32% | 44% | 11% | 61% | 39% |

| WSHP | 2% | 0% | 2% | 6% | 0% | 0% | 0% |

| ASHP | 2% | 3% | 0% | 11% | 11% | 11% | 17% |

| Distributed heat pumps (WLHP) | 22% | 3% | 10% | 17% | 33% | 11% | 28% |

| VRF | 7% | 2% | 7% | 0% | 0% | 11% | 0% |

| Heat Recovery chiller | 8% | 0% | 0% | 11% | 17% | 6% | 17% |

| Non HP measure | 0% | 0% | 2% | 11% | 6% | 6% | 11% |

Table 2 Expressed as percentages

In summary (and for this sample), it seems that

- Bivalent GSHPs were the most commonly assessed system types and were the most likely to have a positive NPV (though only in one-third of the cases examined). They also were the most likely to have the best NPV of the options considered for a specific building (but this was not always positive) and to provide the largest savings and the most savings for a given CAPEX. The cases considered varied widely in the proportion of the peak heating demand that was provided by the GSHP but there was only a very weak relationship between this and the estimated cost and savings. In most cases it was assumed that a gas boiler would provide the top-up, but this is not possible in some locations and oil or electric top=up was also considered. (Any systematic impact from the choice of top-up fuel appeared to be swamped by other factors)

- Distributed heat pump systems (presumably what are known in the UK as water-loop heat pump systems) were also considered relatively frequently – and were already present in some buildings. When they were considered, they were quite likely to have the lowest capex, the largest savings per unit of CAPEX and a positive NPV. Some options appeared to combine ground-coupled heat exchanger with distributed heat pumps”, making the system a “GSHP system”., though this was not always entirely clear (in cases of doubt they have been classified here as GSHP systems)

- VRF systems were considered for a number of buildings and, like distributed heat pump systems, provided the greatest savings in about 10% of buildings for which they were considered (perhaps because both systems share the ability to recover surplus heat from one part of a building for use in other parts.) Unlike distributed heat pump systems, they did not provide the best NPVs (but only a small number of cases considered VRF systems). However, the consultants may not have been familiar with the technology at the time, and other options may have been able to retain more of the existing system.

- Heat recovery chillers were mentioned in several cases, not always as the main element of the package (possibly because they were sized for cooling rather than heating). Where they were the major element of a package, they had relatively low CAPEX but negative NPVs.

- ASHPs were rarely considered (many of the buildings are located in regions where the outdoor temperature falls below -15 C for which ASHPs may have been seen as inappropriate, though bivalent systems and refrigerants that can operate at these temperatures exist. When ASHPs were considered they had negative NPVs, but nevertheless they were sometimes the most attractive (or least unattractive) option. ASHP performance technology, has subsequently improved and “cold climate” products are available.

- There were only two WSHP options assessed. Both had positive NPVs and, from that perspective, good choices for the particular situations – though not the best-rated systems from other perspectives. It is unclear what water sources were considered

While these results provide pointers, it is difficult to generalise from them or to identify features of buildings, their locations, or the existing systems that are reliable indicators of the most suitable or unsuitable options.

The existing systems were predominantly AHU-based (sometimes specifically VAV) central systems, some RTUs, and with a variety of perimeter heating emitters. Heating was mostly by gas or oil boilers but sometimes electric boilers (usually in provinces with low carbon electricity) and occasionally from district steam systems (mostly in the Canadian capital region, Ottawa ON). Cooling was provided by DX units (perhaps not always identified as such) or chilled water chillers.

Comparative analysis of CNS data

An attempt was made to extract meaningful comparisons between systems but this proved to be very difficult and the results should be seen only as broad indications. The 18 buildings in the sample are located in different regions and vary from each other in ways, that are not always reported consistently. The assessments have been carried out by different organisations at different times and it is possible that their assumptions or methodologies may differ. The results below should be seen as indicative and inherently uncertain, since the sample is small compared to the variability of the examples and direct comparison between two given different system types is usually only possible for two or three buildings. This analysis is based on comparisons between different options for the same buildings: this means that the buildings used for each comparison are rarely the same and the results should be viewed as specific indications rather than as being generally applicable. Costs and carbon savings are the designers’ expectations – no information was available on out=turn costs or savings.

Metrics

The options were compared in terms of three metrics: capital cost, annual carbon savings , and (inferred) capital cost of carbon abated – in each case per square metre of floor space. These metrics avoid dependency on energy prices (or time discount rates). The reported carbon savings were converted to a common arbitrary carbon intensity of electricity to reduce the direct impact of the considerable regional differences of intensity. (The choice of systems to be considered for each site will, of course, have been influenced by the actual intensities). No adjustment as been made for climate. Carbon savings were sometimes reported as annual figures and sometimes as 25-year totals: the former have been converted to the latter (with the implicit assumption that the carbon intensity of electricity does not change over this period). No attempt has been made to normalize costs, even though they probably vary between locations and dates (but, of course, they will be comparable for a given building). Other differences between systems, such as maintenance costs, were sometimes reported but have not been analysed. For each characteristic they were compared with the best-performing option considered for each building, resulting in qualitative comparative ratings.

Results

Air Source Heat Pumps were only considered as options for two buildings, it is understood that at the time high-temperature and cold climate models were not available. For these buildings, they ranked highly for capital cost and capital cost of per unit of carbon abated and scored well – but not as highly a some other options) for carbon savings.

Monovalent Ground Source Heat Pumps were rarely considered, scoring highly for carbon savings but rather poorly on capital cost.

Bivalent Ground Source Heat Pumps were more common, with varying proportions of “top-up” rating, provided by either gas or electric boilers – the latter presumably in locations where the electricity supply is low-carbon. The reported (expected) costs and performance were much the same for different proportions of top-up power, though the capital costs were – as would be expected – lower for electric top up. Carbon savings were lower than for monovalent systems and with gas top-up.

Water Source Systems were only considered in two buildings (and the data from one was not useable). Designers are said to be wary about possible biofouling and the clogging of water intakes The (tentative) conclusion is that they can produce carbon savings similar to those of ground source systems but are relatively expensive – but this is likely to be very site-specific.

VRF systems ranked very highly for carbon savings but poorly on capital cost. The high cost is presumably because their use requires replacement of the existing HVAC system. The large carbon savings probably results in part from the ability to recover rejected cooling heat when there is a simultaneous demand for heating and cooling (which will vary with building design and climate).

Distributed (Water Loop) Heat Pump Systems had a broadly similar profile to VRF systems. When used with an electric boiler the savings were slightly lower than for VRF and the cost of abatement was slightly higher. A water loop heat pump system used with a gas boiler was reported as having slightly higher savings than for an electric boiler and therefore a lower capital cost of carbon abatement. This seems to imply (surprisingly) that the carbon intensity of electricity was higher than that of heat from a boiler.

Heat recovery chillers were often mentioned, often in combination with other interventions, making it difficult to identify the costs and savings that related to them. With this proviso, the capital costs appear to be relatively low (possibly because they are the marginal costs compared to a cooling-only chiller)and the carbon reductions comparable to other options.

The CaGBC study took a different perspective, focusing on deep refurbishment packages including fabric improvement, and analysing several building archetypes for different regions of Canada. The focus was also on NPV but here over 40 years, and perhaps using different assumptions about discount rates and fuel prices. The archetypes cover office, multi-unit residential buildings (MURBs), and a primary school and a laboratory. The results were reported in less detail than the CNS study but were presumably more consistent between buildings and regions.

The reports emphasise the value of reducing energy demand, including by fabric improvements, to avoid the need to upgrade heating emitters, to reduce electricity supply requirements and to mitigate space and roof-loading constraints for HVAC equipment and concludes that “…. enclosure upgrades should be considered in the first phase of work, if possible, followed by HVAC upgrades”. They also point out that fabric measures are generally expensive unless there is a need for renewal change for non-energy reasons and that such opportunities are infrequent and “….building condition and renewal schedules may dictate what retrofit strategies are most feasible and cost-effective at a given point in time.” Specifically, for the laboratory archetype fabric upgrades were not cost-effective, but ASHP and GSHP systems were. The report observes that “Retrofits are a tough sell for many building owners – even for cost effective projects – due to a range of economic, market and financial barriers” and has a section devoted to options for procurement methods (for large projects such as deep renovation)

The assumed frequency of replacement of HVAC and fabric elements was summarised as;

- Minor HVAC Equipment such as fans and pumps 10 to 15 years

- Primary HVAC Equipment including boilers, chiller, and rooftop units 15 to 25 years

- HVAC Distribution including pipework, ductwork, heating/cooling terminals, 40 to 60 years

- Windows 20 to 50 years

- Roofs 20 to 30 years

- Walls 50 to 100 years

The descriptions of the HVAC systems that have been assumed to be present in the archetypes and their assumed replacements, provide some market background (and insight into the authors’ thinking). Unlike the CNS study, ASHPs were a mainstay of solutions and GSHPs were mostly ruled out because of assumed restrictions on ground space. GSHPs were considered for the laboratory archetype and were sized to meet the cooling demand rather than the larger heating demand, in order to avoid long-term cooling of the ground and optimise the use of the ground heat exchanger. This resulted in a need for a gas boiler to meet a significant part of the heating load – the GHG reductions for GSHPs were much the same as for ASHPs (as in some of the CNS data).

Specifically:

“Central air-to-water heat pumps were generally chosen to replace oil/natural gas boilers and electrify space heating and service hot water. In a few cases, air cooled variable refrigerant flow (VRF) heat pumps were used ….” For climates that experience temperatures below -15°C (all locations except Vancouver and Halifax), a “peaking” condensing gas boiler was used to satisfy demands at lower temperatures and assumed to provide approximately 1 to 7 per cent of the total heating energy load.” (This seems a very low figure: typical Canadian rules of thumb are that a heat pump sized to handle 30% of the peak heating load can provide 50% of the annual demand over the heating season. At 50% vs peak load => 80% and At 75% => 90+%

Packaged roof top DOAS that were gas fired, with or without DX cooling, were replaced with low ambient DX heat pumps, which are currently capable of -25°C ambient temperatures.

“The most challenging existing HVAC systems to propose low-carbon retrofit solutions for were those that used gas-fired Variable Volume and Temperature, as well as those using Single Zone Constant Volume air handlers….” Solutions included cold-climate DOAS make-up air systems in conjunction with VRF systems, distributed water-to-air heat pumps for zone heating (COP-3.3) and cooling (COP-2.7), and four-pipe fan coil units connected to gas-fired boiler (80% efficient) and air-cooled chiller (COP-2.5). (Note: these COPs seem low)

Dual-duct systems (found in some provinces) were more expensive to upgrade as replacing the dual-duct air handler is much more costly than replacing a smaller air handler and boiler.

Newer buildings (1990s era) were not subject to an enclosure upgrade and it was assumed that heating terminals needed to be upgraded unless they were FCUs. ( High-temperature heat pumps were then a very new concept and do not seem to have been considered)

Retrofit service hot water systems were chosen as a function of annual service hot water demand:

– Low Demand (offices): Local electric resistance domestic hot water (DHW) tanks.

– Low-Medium Demand (primary schools): A dedicated air to water heat pump, supported by an electric resistance boiler.

– Medium Demand (low-rise residential): A dedicated air to water heat pump, supported by a condensing gas boiler. An electric resistance boiler is not considered feasible in this scenario, as this could result in requiring an electrical transformer replacement to meet peak summer electrical loads. – High Demand (mid-rise residential): A wastewater heat recovery heat pump. This option assumes the high demand justifies the cost of installing a wastewater tank in the building basement, and possibly rerouting the waste and sanitary drains to a suitable location as well as installing a heat pump. A small natural gas back-up is used for the approximately 20 per cent of the hot water load that is not available from the building wastewater heat recovery system